A short iron condor is a neutral, defined-risk options strategy that involves selling an out-of-the-money (OTM) call spread and an OTM put spread simultaneously. This strategy profits when the underlying asset's price remains between the short strikes over time, benefiting from time decay. The maximum profit is the initial credit received, while the maximum loss is the width of the spreads minus that credit.

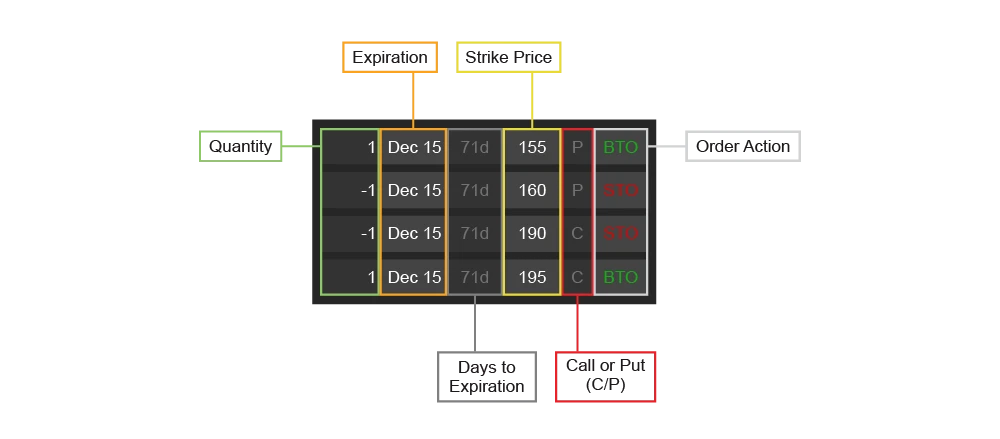

A short iron condor consists of four options forming two short vertical spreads:

Short OTM Call Spread: Sell an OTM call and buy a further OTM call.

Short OTM Put Spread: Sell an OTM put and buy a further OTM put.

This setup provides short exposure to both upside and downside volatility, aiming to profit when the underlying asset remains neutral within the range between the short strikes without significant price movements.

The profit and loss (P&L) diagram of a short iron condor illustrates:

Maximum Profit: The initial credit received, realized if all options expire worthless (i.e., the underlying asset's price stays between the short strikes).

Maximum Loss: The width of the widest spread minus the credit received, occurring if the entire call or put side expires in-the-money (ITM).

Time decay favors short iron condors, potentially yielding a profit before expiration when covered for a debit less than the initial credit received. However, rapid directional moves can offset time decay, leading to losses prior to expiration.

To implement a short iron condor, an investor needs:

Margin Account: Necessary for trading multi-leg options spread strategies like iron condors.

Capital: Sufficient funds to cover the maximum potential loss, which is the width of the widest spread minus the credit received.

Market Outlook: A neutral view, expecting the underlying asset's price to remain between the short strikes until expiration.

Assumptions:

Underlying Asset Price: $100

Short Put Strike: $95

Long Put Strike: $90

Short Call Strike: $105

Long Call Strike: $110

Premiums Received (Short Put and Call): $2 each

Premiums Paid (Long Put and Call): $1 each

In this example, the trader receives a net credit of $2, which is the maximum potential profit. The maximum potential loss is $3, occurring if the underlying asset's price moves beyond the long strikes at expiration.

Executing a short iron condor requires selecting appropriate strike prices and expiration dates to maximize the probability of profit. Follow these steps to structure the trade effectively:

Choose a stock or ETF that you expect to remain range-bound through expiration.

Stocks with low volatility or trading in a sideways pattern work best for this strategy.

Sell an out-of-the-money (OTM) put and sell an OTM call at strike prices where you believe the stock will stay between.

Buy a further OTM put and buy a further OTM call to define risk and limit potential losses.

The wider the distance between the short strikes, the larger the credit received, but the lower the probability of profit.

Sell an out-of-the-money (OTM) put and sell an OTM call at strike prices where you believe the stock will stay between.

Buy a further OTM put and buy a further OTM call to define risk and limit potential losses.

The wider the distance between the short strikes, the larger the credit received, but the lower the probability of profit.

Shorter expirations (e.g., 30-45 days) decay faster and allow quicker profit realization.

Longer expirations (e.g., 60-90 days) provide a slower decay but may offer a higher initial credit.

Shorter expirations (e.g., 30-45 days) decay faster and allow quicker profit realization.

Longer expirations (e.g., 60-90 days) provide a slower decay but may offer a higher initial credit.

Enter the trade as a single multi-leg order, labeled as an iron condor by most brokers.

Use a limit order to control execution price and avoid poor fills.

Track time decay and implied volatility (IV) changes, as they heavily impact the trade’s performance.

If the stock stays between the short strikes, the trade will gradually become profitable.

If the stock price remains within the short strikes, all options expire worthless, and you keep the full premium.

If the stock moves toward a short strike, you may adjust the position or close early to minimize losses.

If the stock breaks out beyond the long strikes, the maximum loss is reached, and closing early may be best.

Theta (Time Decay) Benefits the Trade → As time passes, the short options lose value, increasing the probability of a profit.

Fastest Time Decay Occurs in the Last 30 Days → This is why iron condors are often placed with 30-45 days to expiration.

High IV When Entering is Best – If volatility is high when opening the trade, the credit received will be larger.

Lower IV Benefits the Trade After Entry – A drop in IV reduces the value of the short options, allowing early profit-taking.

If the short put or call is in the money, there is a risk of early assignment before expiration.

To avoid assignment, traders can roll the position forward or close early if the stock moves too close to a short strike.

If the Stock Moves Too Much in One Direction: Consider rolling the challenged spread to a new strike or expiration.

If Implied Volatility Drops: This helps profitability, but a sudden increase in IV can delay profits.

If Profits Accumulate Quickly: Consider closing the trade early when 50-75% of max profit is reached to reduce risk.

| Factor | Short Iron Condor | Iron Butterfly | Straddle/Strangle |

|---|---|---|---|

| Market Bias | Neutral (range-bound) | Neutral (tight range) | High volatility expected |

| Maximum Profit | Limited to initial credit received | Limited to initial credit received | Unlimited for long straddle/strangle |

| Maximum Loss | Width of spread minus credit received | Width of spread minus credit received | Unlimited for short straddle/strangle |

| Time Decay Impact | Positive (profits from decay) | Positive (profits from decay) | Negative for long, positive for short |

| Best Used When | Expecting low volatility | Expecting extremely low volatility | Expecting high volatility |

| Strategy | Best Used When... |

|---|---|

| Iron Butterfly | You expect the stock to stay in a very tight range with less movement. |

| Short Straddle | You want to collect a premium in high IV environments but accept unlimited risk. |

| Short Strangle | Similar to a short iron condor but without defined risk, offering higher credit but greater risk. |

| Credit Spreads | If you want to bet on a specific direction rather than staying neutral. |

The short iron condor is a powerful neutral trading strategy that profits from low volatility and time decay. It works best when:

However, because profits are capped and large price movements lead to losses, this strategy requires careful trade management and risk control.

Since this strategy involves trading both short-term and long-term options, it is ideal for traders who understand volatility, time decay, and expiration risk management.